The 2 Types of Loans Every New Homebuyer Should Know

When you're ready to start house hunting, there are some things you need to look into before you think about floor plans, home locations, and property types. The first being to find out what your actual price range is.

You may already have an idea of what you can afford, but you can't be sure until you secure your proof of funds, which most do through a loan pre-approval.

There are different loan types for you to choose from and pros and cons to each one.

In this blog post, I will give basic information to help you determine which loan is right for you when securing your new home.

The Loans

There are two types of loans that people use to finance their purchases. That's a conventional loan or a government-backed loan.

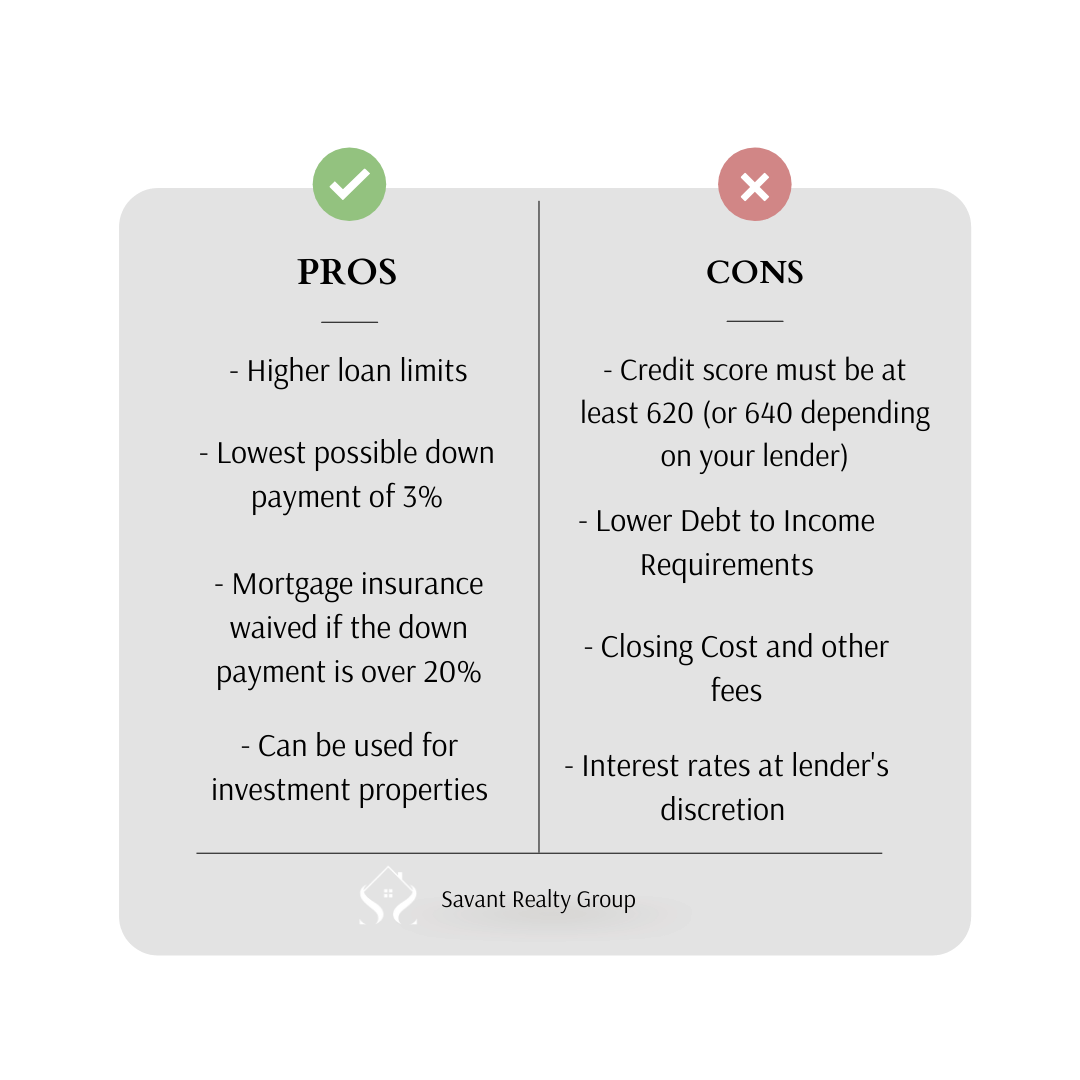

Conventional Loan

A conventional loan is a mortgage loan given by banks or other private lenders and is the most typical loan type for Americans to use. The most beneficial aspect of using this type of loan is the higher loan limits awarded to future homeowners or investors.

The conventional loan is used mainly by individuals with higher credit scores, but you shouldn't be deterred if you don't believe your score is stellar. The conventional loan can be used by anyone with a credit score of 620 or up.

Your credit score makes you eligible for specific pre-approved loan values and interest rates. Therefore an applicant with a higher score may be awarded a higher loan and lower interest rates.

Below is a complete list of the pros and cons of using a conventional loan.

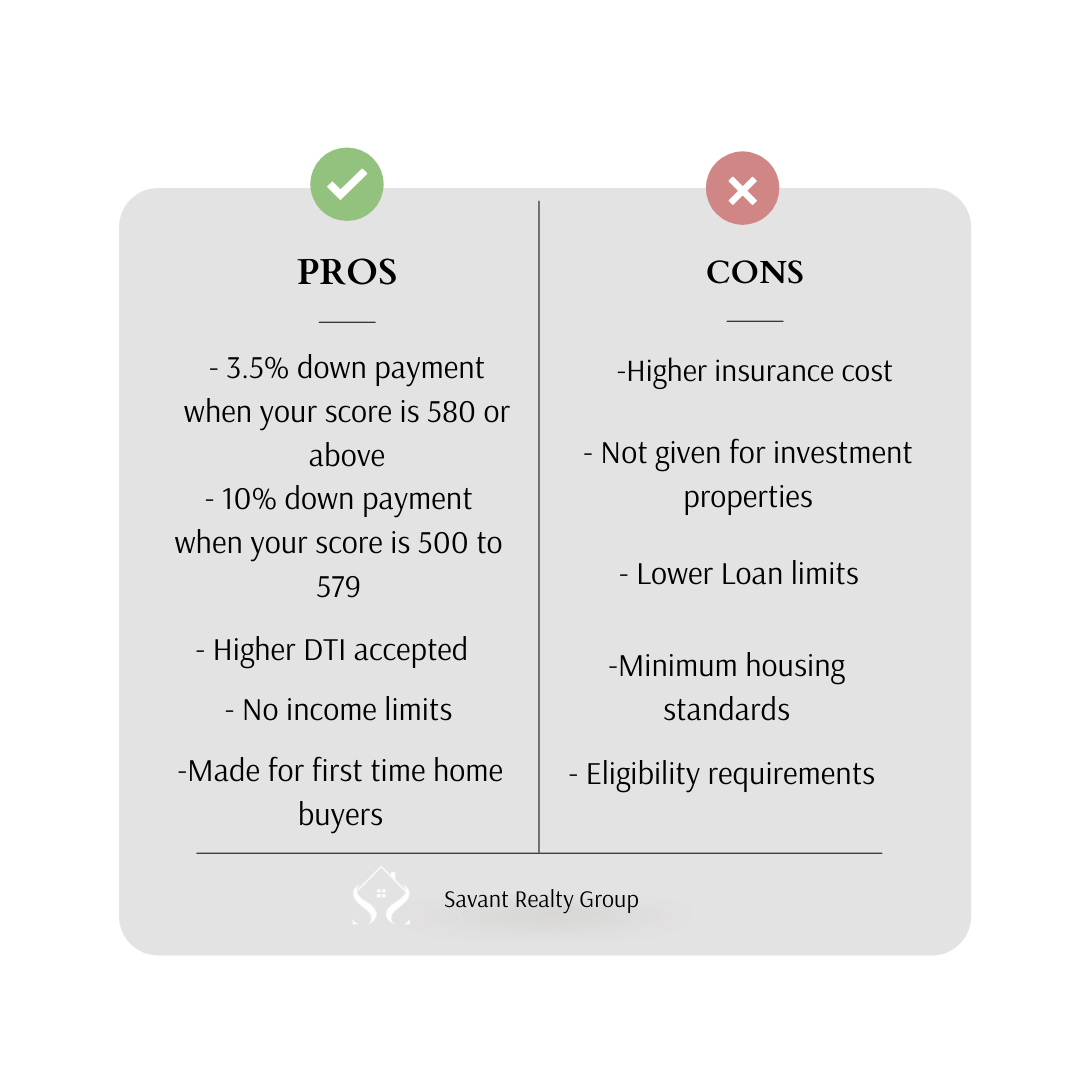

Government-Backed Loan

Government-backed loans are loans that are insured by the government and offered by private lenders. When lenders award government-backed loans, they are protected if the recipient doesn't pay back the amount owed.

Many government-backed loans are for homeowners to choose from, but the most used is the FHA loan.

The FHA loan is given by the Federal Housing Administration, which the loan is named after. It is popular amongst first-time homebuyers or individuals with low credit looking to buy a home.

Below is a complete list of the pros and cons of using an FHA loan.

Pre-Approval

I've thrown the word "pre-approval" around throughout this post, and you may not know what it means.

It's when a lender (an organization that gives out loans) approves you for a certain amount of money before actually giving it to you.

Receiving this number is essential to making your offers more competitive, especially in this saturated market.

Pro tip: It's best if you use lenders that your realtor recommends. The relationship your realtor has built with these lenders allows for your pre-approval to be done in a more accurate and timely manner than when doing it yourself.

Conclusion

When determining which type of loan is right for you, you should consider your credit score, the down payment you have on hand, and whether the property is a primary home or an investment. These three things should give you a clear idea of what type of loan you should acquire.

Of course, speak to a realtor to help guide you in the right direction. To talk to Shood Realtor or any of our Savants, click here, and we will get in contact with you.

Categories

- All Blogs (659)

- Affordability (16)

- Agent Value (27)

- Baby Boomers (8)

- Buyers (437)

- Buying Myths (117)

- Buying Tips (49)

- Credit (3)

- Demographics (32)

- Distressed Properties (6)

- Down Payment (23)

- Downsize (2)

- Economy (16)

- Equity (12)

- Family (2)

- Featured (8)

- First Time Homebuyers (211)

- For Sale by Owner (1)

- Forecasts (7)

- Foreclosures (28)

- FSBOs (11)

- Gen X (1)

- Gen Z (5)

- Home Improvement (2)

- Home Prices (37)

- Housing Market Updates (231)

- Interest Rates (70)

- Inventory (30)

- Investing (6)

- Kids (2)

- Leasers (6)

- Lenders (4)

- Loans (8)

- Luxury Market (3)

- Market (3)

- Millennials (9)

- Mortgage (18)

- mortgage rates (31)

- Move Up Buyers (84)

- New Construction (13)

- Pricing (95)

- Rent v. Buy (36)

- Self-Employed (1)

- Sellers (292)

- Selling Myths (87)

- Selling Tips (40)

- Senior Market (1)

Recent Posts

GET MORE INFORMATION

Agent | License ID: 740140